Market Commentary: 50x All Time High!

By Brian Andrew, CFA® – Chief Investment Officer

Please join me in remembering our Veterans on this Veterans Day. At Merit we celebrate their contributions and especially appreciate their sacrifices.

As we closed out election week, the S&P 500 Index price was almost at 6,000 and the DJIA almost 44,000. This was the 50th all-time-high (ATH) for the S&P 500 Index this year! Not only did we see a post-election relief rally last week, we also saw new enthusiasm for taking risk across markets.

Financial stocks, bitcoin, and the tech heavy NASDAQ index hit an all-time high. These animal sprits come from several sources so let’s review those and determine what this means going forward.

Post-election

We’ve pointed out in previous communication that markets tend to rally after a presidential election through the end of the year. This result stems from the removal of the uncertainty of the outcome. However, this go around, we not only had the removal of the uncertainty, but an outcome that was viewed to have a probability. The win by former President Donald Trump, Republicans securing control of the Senate and potential for the House was viewed by investors to change the trajectory of several policies.

Of course, it is too early to know what those policies will specifically be, however, not too early to do what markets do best, speculate.

One of the reasons for the boost to financial stocks comes from the idea that we could see less regulation on the financial services industry. Regulation comes with a cost and so investors perceive a better time ahead for operating margins. Couple that with the benefit banks get from bigger yield spreads between their assets and liabilities and you can see the opportunity. Goldman Sachs was up 11% the day after the election while JP Morgan was up almost 9%.

The other que investors picked up on was the potential for a more favorable change in tax policy. While the 2017 TCJA provided lower corporate tax rates, it comes due in 2025. Investors assume that most of what is in that Act that benefitted corporations will be rolled over or improved upon. While likely true, we should be careful not to extrapolate too much benefit as there are still budget hawks in the Republican Party who will fight back against raising the deficit if the tax proposals aren’t paid for.

Economy

Investors have been reading the tea leaves of economic data and instead of looking for signs of weakness, looking for strength. Last week, when the Institute of Supply Management for Services was released the data showed a move higher into expansionary territory. In addition, the Services Employment portion of the data also went up suggesting a better employment environment among service sectors.

Quarter over quarter labor costs actually declined suggesting that the market for people and the jobs available is stabilizing reducing inflationary forces.

Finally, the Federal Reserve met last week and during Chairman Powell’s press conference he noted that some businesses are “indicating that next year could be even stronger than this year…”

Federal Reserve

At that meeting of the Fed, they decided to reduce interest rates by .25% discussing the fact that they see a balance between inflationary forces and economic improvement. Most inflation measures have been trending toward their 2% target.

While true, the election will provide the Fed with insight into how Americans are feeling about inflation. They don’t see it as a battle won because while the rate of price increases has declined, the actual level of prices remains high due to stimulus demand and prior logistics bottlenecks.

At the press conference, Chair Powell reiterated that the Fed is “on the path to a more neutral stance,” which we take to mean that short-term interest rates will continue to follow the Federal Funds rate lower in the coming months.

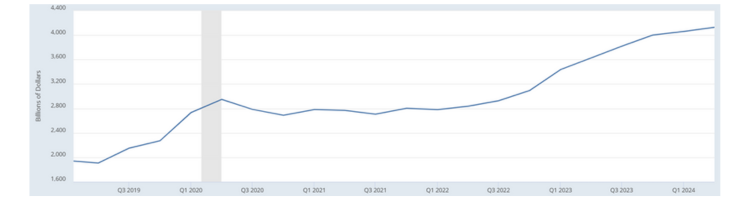

Cash Move

Many investment pundits have noted the large amount of cash in money market funds as a potential benefit for markets. The thought is that more certainty about the future path of government policy and improvement in economic data will pull investors cash into markets pushing prices even higher. As you can see from the chart here total money market fund balances for households and nonprofit organizations is over $4 trillion.

Source: Federal Reserve of St. Louis, Board of Governors of the Federal Reserve System

You can see that this balance hasn’t declined yet, suggesting that despite the market’s ATH’s we’re still waiting for individual investors to move their cash into the market.

Of course, we can’t predict when that will happen though given the improvement in market sentiment it seems like it could be more likely.

Hailing from a Swing State, I can say that I’m glad we’ll have a reduction in political advertising and look forward to assessing the future moves of the new Administration and Congress as we move into 2025.