2025 Investment Outlook: Navigating Inflation, AI, and Policy Shifts for Sustainable Growth

By Brian Andrew, CFA® – Chief Investment Officer

2024 Recap: The Economy Has Landed

Over the past two years, discussions around a potential U.S. recession or soft landing dominated economic outlooks. Now, as 2024 concludes, it is evident that the economy has achieved a soft landing. Government spending played a key role in supporting economic growth and sustaining a stronger labor market than anticipated. Additional contributors included the reshoring of manufacturing and increased investment in artificial intelligence (AI) infrastructure. Below, we review how 2024 ended and highlight five critical areas of focus for 2025.

2024 Performance

The U.S. economy grew by 2.7% (after inflation) from September 2023 to September 2024, with the Atlanta Fed GDPNow forecasting a 3.1% growth rate for Q4 2024. Projections for 2025 suggest growth exceeding 2%, supported by improved consumer sentiment tied to expectations of a new Republican-led government delivering favorable changes in inflation, taxes, and trade policies.

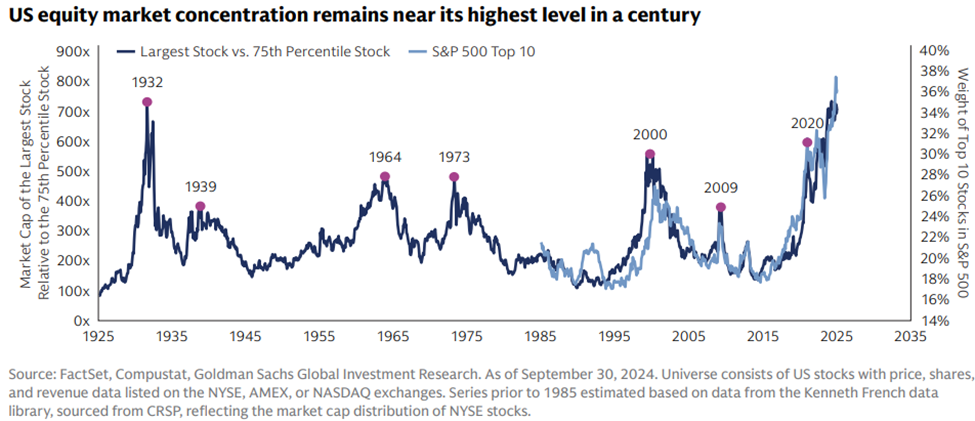

The S&P 500 Index delivered an impressive 23% return in 2024, while the technology-centric NASDAQ surged over 30%. Despite these gains, market performance remained narrow, with a handful of stocks driving the majority of returns. International equities lagged U.S. markets due to weaker economies and lower exposure to technology-focused industries.

The Federal Reserve cut the Federal Funds rate by 1% over the year, offering a tailwind to investors. Core PCE inflation decreased to 2.6% by mid-year, down from its peak of 5.6% in September 2023. However, as Q4 progressed, inflation ticked slightly higher to 2.8%, tempering expectations of rapid rate reductions in 2025. Interest rates began normalizing, with 10-year Treasury yields rising modestly while 2-year rates held steady.

Artificial intelligence emerged as the dominant secular theme in 2024. Key beneficiaries included major tech firms such as Microsoft, Meta, Google, and Amazon, as well as chip suppliers like Nvidia and Broadcom. The growing demand for electricity to power AI infrastructure also highlighted broader opportunities within the AI ecosystem.

2025 Market Outlook: Five Key Areas of Focus

1. New Government: President-elect Donald Trump is set to take office on January 20th, initiating a whirlwind of policy developments. Key areas to monitor include government spending, trade, immigration, taxes, and regulation:

- Spending: Congress must address the budget and debt ceiling by mid-March.

- Taxes: With the 2017 tax cuts expiring at the end of 2025, a new tax bill is expected, although it may take time to pass.

- Trade: Tariff adjustments, which do not require Congressional approval, could be enacted quickly, potentially reshaping negotiations.

- Immigration: Executive orders may lead to progress on border policies, especially as rising unemployment creates opportunities for compromise.

- Regulation: A less stringent regulatory environment is likely, benefiting financial systems, energy, and tech infrastructure.

2. Federal Reserve and Inflation: The Federal Reserve cut rates by 0.25% in December, signaling a more cautious pace of easing in 2025. Decisions will hinge on metrics such as unemployment, personal income, consumption, and core inflation trends.

3. Interest Rates: Interest rates remain a pivotal factor for consumers, businesses, and asset valuations. In 2025, short-term government rates are expected to decline modestly, while long-term rates may edge higher, reflecting a stronger economic outlook and increased debt issuance. Corporate bonds could offer attractive yields as companies refinance maturing debt at higher rates, presenting opportunities for bond investors.

4. Stock Prices and Earnings Growth: While technology companies led earnings growth in 2024, broader economic improvements and potential tax cuts may drive stronger performance across mid-size and smaller companies in 2025. International equities, particularly in developed Europe, are expected to underperform U.S. markets, as geopolitical and tariff uncertainties weigh on their outlook. Emerging markets may face challenges from a strong U.S. dollar but could still offer selective opportunities.

5. Secular Themes: Long-term economic and market drivers will continue to shape opportunities:

- Demographics: The U.S. benefits from a growing 18-34 age cohort, bolstering economic activity.

- Infrastructure: Ongoing government investment supports long-term economic growth and investor opportunities.

- Artificial Intelligence: The AI boom continues, with initial benefits focused on infrastructure such as microchips, servers, and data centers. Over time, broader adoption is expected to benefit additional companies beyond 2024’s tech giants.

- Geopolitics: A shift toward nationalist policies globally may impact trade, inflation, and asset prices, requiring careful portfolio construction.

As 2025 unfolds, these five areas will guide our investment strategies, ensuring readiness to capitalize on opportunities while managing potential risks.

2025 Equity Market Outlook: Resilience Amid Elevated Risks

2024 Recap: Equity markets in 2024 were buoyed by a momentum-driven rally in growth stocks. While the first half of the year saw outsized gains from mega-cap technology firms, the rally broadened in the latter half, spurred by improving economic data, easing monetary policies, and optimism over potential political shifts favoring a Republican-led government. Despite these tailwinds, international equities lagged, constrained by slower economic growth, persistent risks in China, and global geopolitical tensions.

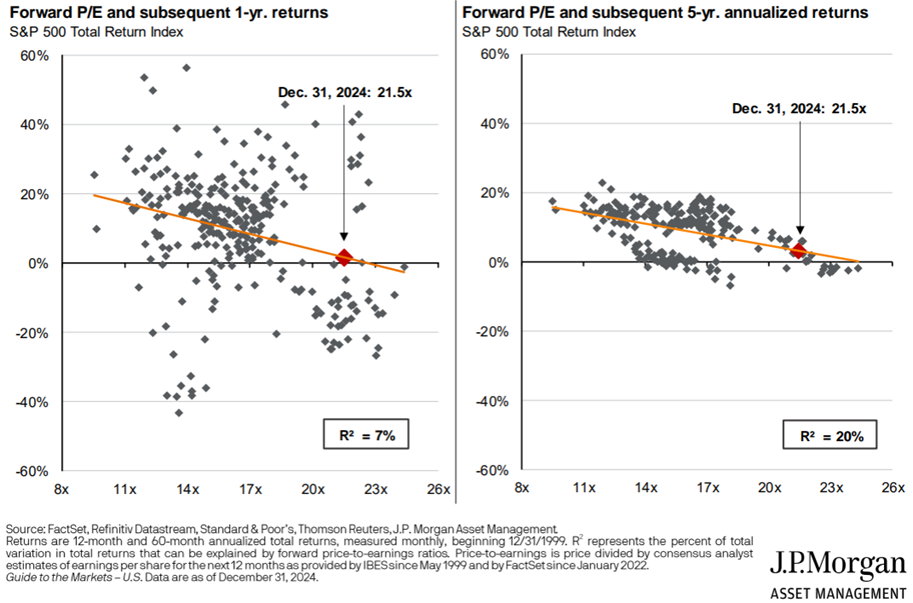

As we enter 2025, equity markets stand on solid footing, underpinned by strong economic fundamentals and resilient earnings growth. However, elevated valuations remain a concern. Should economic or earnings growth disappoint, market volatility may increase, particularly if heightened valuations face downward pressure. Additionally, activity pulled forward into late 2024 due to tariff-related uncertainties could dampen early 2025 growth prospects.

To mitigate these risks, investors are encouraged to rebalance portfolios, aligning with long-term allocation targets. This strategy can help capture gains from equities while leveraging attractive bond yields and the potential for falling interest rates.

Positive Catalysts:

- Private Investment Cycle: Accelerating private capital expenditure, particularly in AI, cloud computing, and renewable energy, is poised to drive economic growth.

- Consumer Strength: Resilient consumer balance sheets and a robust labor market provide a strong foundation for continued consumer spending.

- Earnings Growth: Domestic earnings growth is projected to accelerate to 12.5% in 2025, up from 8.3% in 2024, with broader sector participation expected to drive diversified market returns.

Risks to Watch:

- Valuation Concerns: The S&P 500’s forward P/E ratio stands at 22.2x, above its historical average, posing potential headwinds if earnings or economic growth underperform.

- Geopolitical Tensions: International risks, including China’s decelerating growth and EU inflation challenges, could further pressure global equity markets.

Strategic Focus: Investors should emphasize quality and value stocks, particularly as growth stock valuations remain elevated. Value-oriented strategies not only offer relative affordability but also stand to benefit from broader economic growth. Additionally, low-volatility strategies can act as portfolio hedges against valuation-driven pullbacks.

Opportunities: Domestic and International Perspectives

U.S. Market: Strong private-sector investment in AI and infrastructure, coupled with improved productivity, positions the domestic market for sustained growth. AI is expected to enhance productivity across industries, ranging from service sectors to biotechnology. These innovations offer long-term secular growth themes, particularly as infrastructure build-outs gain traction.

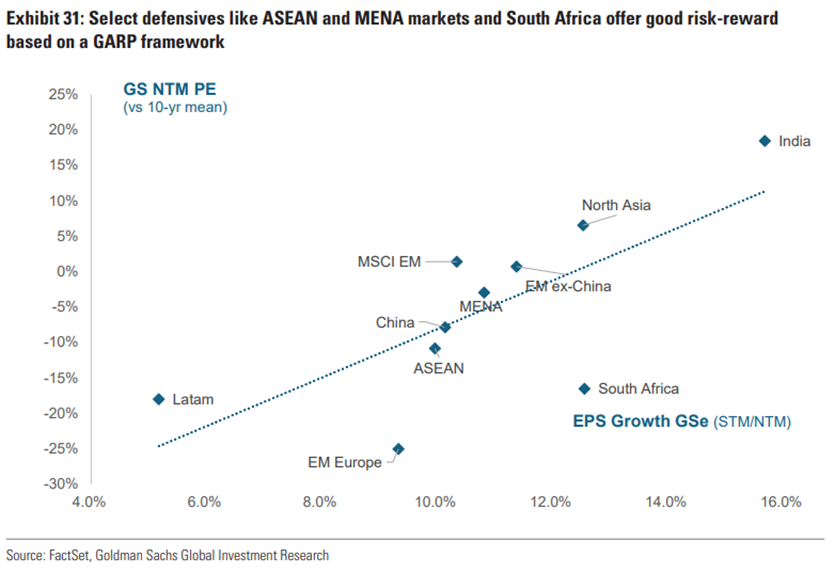

International Equities: Opportunities abroad remain selectively compelling despite lower valuations and persistent risks. Europe, particularly Germany, struggles with below-trend growth and energy-driven inflation stemming from the Russia-Ukraine war. This environment has led to cautious consumer behavior, further dampening economic growth. Emerging markets present a mixed outlook, with Southeast Asia benefiting from growth-friendly policies, while commodity-reliant economies face headwinds from weaker global demand.

China’s Deceleration: China’s GDP growth is projected to slow to 4.5% in 2025, presenting challenges for resource-dependent emerging markets. However, regions with resilient domestic demand and structural growth drivers, such as renewable energy and digital transformation, remain attractive for active investors.

2025 Fixed Income Outlook: Balancing Yield and Volatility

2024 Recap: The past year was characterized by a robust economy and resilient consumer activity, supported by an improving inflation backdrop and strategic Federal Reserve actions. Interest rate fluctuations defined the year, with domestic rates experiencing over a 100-basis-point range of volatility amid speculation on Fed policy. Notably, the two-year Treasury yield ended 2024 near its starting point, underscoring market unpredictability.

The Federal Reserve held off on rate cuts until late 2024, initiating a 50-basis-point reduction in September. This marked the beginning of the long-anticipated easing cycle and reflected a strong U.S. economy and labor market. However, the Fed’s “higher for longer” approach persists into 2025, despite short-term rates being 100 basis points lower than at the start of 2024.

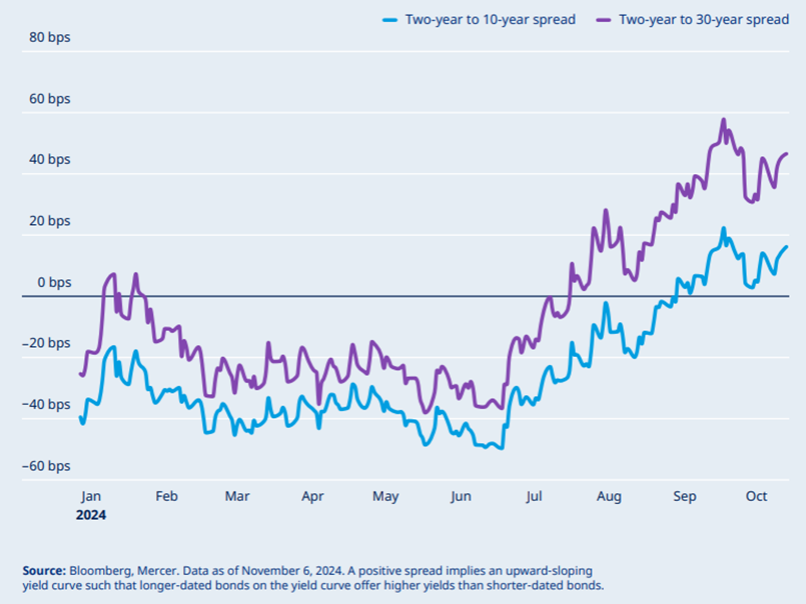

Shifts in the Yield Curve: The yield curve underwent a significant adjustment in 2024. Initially inverted by nearly 50 basis points during the summer, the curve steepened to a positive spread exceeding 20 basis points by year-end. This transition presents opportunities to extend duration, though risks from increasing term premiums remain. (Term premium refers to the additional compensation investors require for holding longer-term bonds, reflecting uncertainty about future economic conditions and interest rates.)

A decomposition of yield increases highlights term premiums as the primary driver, with inflation playing a secondary but significant role. Fiscal policy under the new administration, coupled with potential tariffs, could exert further upward pressure on term premiums.

Constructive Backdrop for Fixed Income: Despite potential volatility, fixed income markets present compelling opportunities in 2025. Yields on high-quality securities in the 5-6% range offer an attractive entry point. Elevated rates are expected to persist as the Fed slows its easing pace and the Federal government refrains from addressing budget deficits. Additionally, strong corporate fundamentals, fueled by consumer spending, support growth trends and provide further stability.

Corporate bond yields remained tight relative to Treasuries in 2024, with High Yield credit outperforming Investment Grade. Strong fundamentals suggest limited risk of meaningful spread widening in 2025. Robust investor demand continues to drive a healthy new issue market, while corporate balance sheets remain resilient, aided by productivity gains from AI advancements.

High Yield and Securitized Opportunities: Defaults in High Yield remain near historic lows, with BB-rated credits now dominating the market—a shift from lower-quality, unprofitable issuers of the past. Attractive relative value opportunities persist in corporate credit heading into 2025.

Securitized spreads also present value, particularly in mortgage-backed securities. High-quality AAA-rated securitized paper is now priced closer to BBB or High Yield corporate credit, offering a cushion against spread widening and potential price appreciation if relationships normalize.

Positioning for 2025: Tight spreads, alongside elevated Treasury yields, create a favorable environment for real returns. Unlike 2022’s negative real yields, current conditions offer opportunities to achieve high levels of income while maintaining portfolio stability. Fixed income is well-positioned to provide the ballast investors seek, remaining a cornerstone of diversified portfolios throughout 2025.

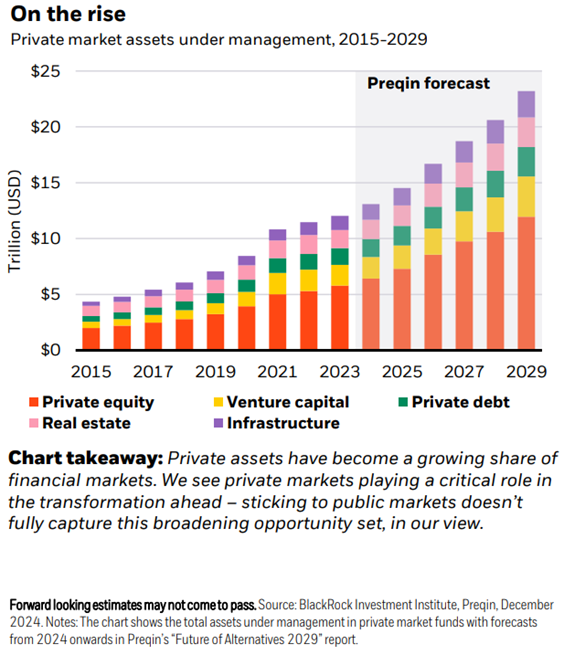

2025 Alternative Income Outlook: Enhancing Diversification and Risk Management

2024 Recap: The alternative investment landscape in 2024 showcased resilience despite macroeconomic uncertainties, geopolitical tensions, and elevated interest rates. Hedge funds delivered mixed results, with equity-focused strategies underperforming due to market volatility, while multi-strategy and market-neutral funds excelled as investors sought diversification and uncorrelated returns. These strategies underscored their significance as tools for managing risk in unpredictable environments.

Private equity experienced subdued deal activity, as higher borrowing costs constrained valuations and access to capital. However, sectors such as technology, healthcare, and renewable energy continued to attract strong capital flows due to their long-term growth potential. Private credit emerged as a standout performer, offering yields that exceeded traditional fixed income. First-lien and senior-secured lending dominated, providing compelling risk-adjusted returns in a high-rate environment.

Real estate markets began to stabilize, particularly in industrial and multifamily properties, which benefitted from robust demand fundamentals and inflation-linked cash flows. Conversely, the office and retail sectors struggled with structural challenges, including evolving work habits and shifting consumer behaviors. Infrastructure investments gained momentum, driven by global energy transition initiatives, digital infrastructure demands, and government-backed expenditures. Meanwhile, Bitcoin and other digital assets rebounded, bolstered by growing institutional adoption and improved regulatory clarity.

Public equity markets remain at extended valuations. As we enter 2025, the alternative investment landscape appears poised for growth, supported by improving macroeconomic conditions, moderating interest rates, and sector-specific tailwinds. Below is a detailed outlook for key asset classes.

Hedge Funds: Positioning for Volatility and Alpha

Hedge funds are expected to thrive in 2025, leveraging their adaptability in volatile markets and amid macroeconomic uncertainties. Multi-strategy funds remain a top choice for their diversification benefits, blending uncorrelated strategies to deliver consistent returns. Equity market-neutral funds and relative value strategies are gaining traction, well-suited to exploit inefficiencies in uncertain markets. These approaches could appeal to investors concerned about high public equity valuations.

Event-driven strategies, particularly those focused on mergers and acquisitions (M&A), are anticipated to gain traction as corporate activity rebounds. Companies are likely to pursue strategic transactions to drive growth and adapt to shifting market dynamics. Fixed income arbitrage strategies also stand out, positioned to deliver alpha as investors seek opportunities in higher-yielding assets.

Private Equity: A Focus on Resilience and Growth

Private equity is poised for recovery in 2025, driven by improved financing conditions and stabilization in valuations. The mid-market segment offers appealing entry multiples and reduced competition compared to larger buyouts. Technology, healthcare, and infrastructure sectors are expected to dominate deal flow, reflecting robust demand for innovation and essential services.

General partners are increasingly prioritizing operational improvements and value creation to ensure portfolio resilience amid economic uncertainties. Strategies emphasizing these approaches, rather than financial engineering, are favored. Secondary funds continue to gain momentum as investors seek liquidity and access to mature, de-risked assets, presenting a valuable avenue for reallocating capital and achieving diversified returns.

Private Credit: Sustaining Yield Leadership

Private credit remains a cornerstone of alternative investment portfolios in 2025, particularly for income-focused investors. First-lien and senior-secured lending are expected to lead, offering attractive yields and downside protection. With default rates inching up in select sectors, distressed credit strategies are likely to gain prominence, providing tactical opportunities for skilled managers.

The competitive landscape in private credit is intensifying as traditional fixed income instruments offer improved yields. This dynamic underscores the need for disciplined underwriting and a focus on high-quality borrowers. Private credit’s flexibility continues to attract investors, enabling tailored risk exposures to align with specific market conditions.

Infrastructure: Benefiting from Secular Trends

Infrastructure investments are well-positioned for growth in 2025, supported by secular trends such as global energy transitions, digital infrastructure expansion, and urbanization. Government and private sector spending will drive projects, particularly in renewable energy, including wind and solar, as countries pursue carbon neutrality goals. Digital infrastructure, encompassing data centers and broadband networks, remains a focal point due to surging e-commerce and AI-related demands.

Transportation infrastructure, including highways and rail networks, also presents opportunities as governments prioritize spending to stimulate economic growth. Infrastructure assets continue to offer stable, inflation-linked cash flows, making them appealing to long-term investors seeking income and diversification.

Real Estate: Stabilization with Diverging Trends

Real estate markets are expected to stabilize further in 2025, although sector performance will vary. Industrial and multifamily properties remain resilient, driven by strong demand fundamentals, steady rent growth, and inflation-adjusted leases. These sectors continue to attract institutional capital for their reliability and growth potential.

Office and retail properties face ongoing challenges, including reduced demand from hybrid work models and shifting consumer preferences. However, years of underperformance and declining returns may create tactical investment opportunities, especially in well-located and adaptable assets. Emerging opportunities in data centers and logistics facilities tied to e-commerce and AI infrastructure also highlight growth areas for strategic investors.

Bitcoin and Digital Assets: Growing Institutional Acceptance

Bitcoin continues to gain traction as a portfolio diversifier, with its low correlation to traditional assets making it an appealing hedge against market volatility. Institutional adoption is rising, driven by political support, enhanced regulatory clarity, and an expanding digital asset ecosystem. Developments in decentralized finance (DeFi) and asset tokenization present new growth avenues, although these innovations require robust risk management due to inherent volatility.

Investors are also exploring thematic allocations to blockchain technologies, recognizing their potential to disrupt industries and create long-term value. However, prudent allocation and understanding of risks are crucial when incorporating digital assets into portfolios.

Structured Products: Falling Yields and Volatility

Structured products demonstrated strong risk-return characteristics in 2024’s environment of high interest rates and elevated market volatility. These conditions allowed market-linked income notes to deliver double-digit coupon rates, appealing to income-focused investors. As yields decline and public market volatility moderates in 2025, the appeal of structured products may soften slightly but remains competitive for unique, risk-adjusted returns.

Structured products, particularly market-linked growth and income notes are expected to continue complementing investment portfolios in more stable economic conditions.

Strategic Allocations for 2025: Opportunities in Diversification

A diversified investment strategy incorporating equities, fixed income, and alternatives offers the best approach to capture growth and manage risks in 2025. By focusing on key themes—government policy changes, Federal Reserve actions, interest rate trends, earnings growth, and secular trends—investors can maintain balanced and resilient portfolios.

Equities: Policy-driven spending, tax changes, and innovation in AI and infrastructure will support growth. Mid-size companies and value-driven sectors like healthcare and renewable energy offer strong potential, while international equities face mixed prospects due to trade and currency headwinds.

Fixed Income: High-quality securities yielding 5-6% present attractive opportunities. Short-term rates may decline, while long-term yields could edge higher, benefiting corporate bonds and securitized credit. Fixed income provides stability and income amid gradual Fed easing.

Alternatives: Alternatives encompass hedge funds, private equity, private credit, infrastructure, and digital assets, offering diversification and resilience. Hedge funds are poised to capitalize on volatility and inefficiencies, while private equity focuses on high-growth sectors such as AI, renewable energy, and infrastructure. Private credit delivers strong yields and downside protection, supported by disciplined underwriting. Infrastructure investments benefit from secular trends in energy transitions and digital expansion, offering stable, inflation-linked cash flows. Additionally, digital assets like Bitcoin and blockchain-related technologies present thematic growth opportunities and portfolio diversification.

By aligning allocations across these asset classes and monitoring policy developments, investors can optimize returns and mitigate risks in a dynamic global market. Diversification remains essential for achieving sustainable growth and resilience in 2025.